Corporate Income Tax (CIT)

General tax rates:

Standard tax rate: Most companies in Vietnam are subject to a standard corporate income tax rate of 20%. This rate is applied to the company’s annual taxable income and is the main basis for the company’s tax burden.

Preferential tax rates:

10% preferential tax rate: Investment projects in certain industries or regions may enjoy a preferential tax rate of 10%. This preferential tax rate usually applies to industries that are given priority support by the government, such as high-tech industries, environmental protection projects, agricultural projects, and investment projects in economically backward areas. The preferential period can be up to 15 years, depending on the nature and scale of the project.

17% preferential tax rate: Certain qualified investment projects can enjoy a preferential tax rate of 17%, with a preferential period of up to 10 years. Projects subject to this tax rate usually include start-up investments in small and medium-sized enterprises, some manufacturing projects, and investment projects that are in line with the national industrial policy orientation.

Oil exploration and development: Enterprises engaged in oil exploration and development are subject to corporate income tax rates ranging from 32% to 50%. This high tax rate reflects the high profitability and resource scarcity of the oil industry, and is also intended to regulate the distribution of resource development benefits between the state and enterprises.

Exploration and mining of precious and rare natural resources: For enterprises engaged in the exploration and mining of precious and rare natural resources, the applicable corporate income tax rate is 40% to 50%. Such resources include rare minerals, metals, etc. The tax rate is set not only to increase national revenue, but also to control the over-exploitation of resources and protect the environment.

Personal Income Tax (PIT)

Progressive tax rates (applicable to tax residents)

Progressive tax rates (applicable to tax residents):

Tax residents, i.e. individuals who reside in Vietnam for more than 183 days, have their income taxed at progressive rates, ranging from 5% to 35% depending on the level of taxable income.

Flat tax rates for other types of income:

Certain types of income of tax residents are subject to fixed tax rates. These types of income and corresponding tax rates are as follows:

Capital investment income: The tax rate applicable to capital investment income is 5%. Capital investment income includes dividends, interest and other forms of investment income.

Capital transfer income: Capital transfer income is taxed at 20%. This generally applies to income from the sale of shares, equity or other capital assets.

Securities Exchange Gains: A flat tax of 20% is levied on securities exchange gains, which applies to profits derived from the purchase and sale of stocks, bonds or other securities.

Income from the transfer of real estate: Income from the transfer of real estate is taxed at two rates: 2% of the transfer amount or 25% of the taxable income, whichever is higher. This includes income from the sale or transfer of real estate such as houses and land.

Royalty income: The tax rate for royalty income is 5%, which applies to income obtained by licensing others to use patents, trademarks, copyrights or other intellectual property rights.

Royalty income: The 5% tax rate also applies to royalty income, which involves income from licensing others to use technology, brands or business models.

Bonus income: A fixed tax rate of 10% is levied on bonus income, which usually includes various forms of rewards, such as year-end bonuses, performance awards, etc.

Inheritance and gift income: Property acquired through inheritance or gift is subject to a 10% tax. This applies to all inheritances or gifts received in Vietnam.

Rental income: Rental income is subject to a flat tax rate of 10%. This includes rent received from renting out residential property, commercial property, or other real property.

Value Added Tax (VAT)

Three tax rates apply:

Vietnam’s VAT system applies three different tax rates, which are classified and taxed according to the nature of goods and services and policy orientation.

0% Tax Rate:

Applicable to export goods and services, including goods sold by Vietnamese enterprises to the international market, international transportation services provided, cross-border services, etc. This tax rate is intended to encourage exports, enhance the competitiveness of Vietnamese enterprises in the international market, and avoid double taxation of export goods.

5% tax rate:

Applicable to specific necessities and services. Usually including goods and services related to basic life, such as some food, medical equipment, medicines, books, cleaning utensils, agricultural machinery, etc. This preferential tax rate is aimed at reducing the tax burden on basic consumer goods and services, safeguarding people’s livelihood needs, and promoting balanced economic development.

10% tax rate:

This is the standard tax rate applicable to most goods and services, including consumer goods, luxury goods, general services, manufacturing products, etc. The 10% tax rate is the base tax rate for VAT in Vietnam, which applies to all goods and services without special provisions, ensuring the stability of government fiscal revenue.

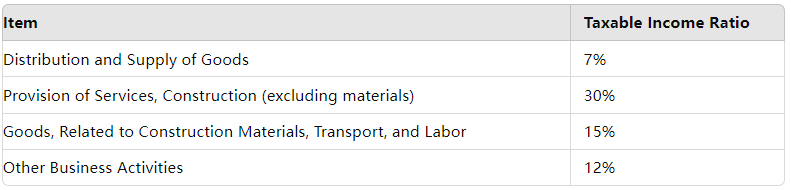

Foreign Contractor Tax

Taxable income ratio

Foreign contractor tax is a tax imposed on foreign contractors doing business in Vietnam. The taxable income percentage varies depending on the type of business, but generally includes the following main business categories:

Service provision and leasing:

For services provided by foreign contractors (including consulting, technical services, etc.) and leasing activities, the taxable income ratio is usually 5% to 7%. This means that 5% to 7% of the foreign contractor’s total income is deemed as taxable income, and taxes are calculated and paid accordingly.

Sales of goods and ancillary services:

If a foreign contractor not only sells goods but also provides services related to the goods (such as installation, training), the taxable income ratio is usually 1% to 3%. In this case, contractor tax is only levied on the service part, and the goods sales part is usually not included in the taxable scope.

Construction and installation:

In cases involving construction, installation or engineering contracts, the taxable income percentage is usually between 2% and 3%, depending on the nature and content of the contract.

Other business activities:

For other types of business activities, the proportion of taxable income of foreign contractors may be different, and the specific proportion is assessed and determined by the Vietnamese tax department based on the type of business and the terms of the contract.

Tax incentives

Tax holidays and tax reduction policies:

Tax exemption period:

Eligible companies can enjoy a 2-4 year tax holiday, during which their taxable income will be completely exempted, providing an important tax buffer for newly established or expanding companies.

Tax reduction period:

After the tax exemption period ends, enterprises can enjoy a 50% reduction in corporate income tax for the next 4-9 years. This means that during this period, enterprises only need to pay half of the tax payable, which will help enterprises further consolidate their market position and development potential.

Applicable industries:

The Vietnamese government offers tax incentives to specific industries to encourage development and investment in these areas:

Education: includes educational programs such as schools and vocational training institutions.

Healthcare: Businesses involved in hospitals, clinics, and other healthcare services.

High technology: such as information technology, electronic product manufacturing and advanced manufacturing technology.

Environmental Protection: Projects dedicated to environmental protection and sustainable development, such as pollution control and clean energy projects.

R&D: Focus on research and development of new technologies and innovative products.

Infrastructure development: including the construction and operation of projects such as transportation, energy, and water conservancy facilities.

Agricultural product processing: involves the processing and value-added services of agricultural products.

Software Development: covers software design, development and related IT services.

Renewable energy: such as wind energy, solar energy, biomass energy and other new energy projects.

Applicable regions:

Tax incentives are also particularly applicable to the following areas to promote economic development in these areas:

Underdeveloped regions: usually regions in Vietnam where the economy is relatively backward and urgently need to attract investment and promote regional development through tax incentives.

Border areas: The border areas where Vietnam borders with neighboring countries, which usually need to strengthen infrastructure construction and economic vitality.

Special Economic Zone: A special economic zone or free trade zone designated by the government, which aims to attract foreign investment and technology through special economic policies and tax incentives and promote rapid development of the regional economy.